“Buy the dip” sounds like the kind of investing advice that belongs on a coffee mug, a gym shirt, and possibly a very confident uncle’s Facebook post. The idea is simple: when a stock, ETF, or the overall market drops, you buy at the lower price and wait for the rebound. In theory, it is bargain hunting. In practice, it can feel like trying to catch a bowling ball with oven mitts.

So, does buy the dip work? The honest answer is: sometimes, but not automatically. Buying a dip can work when the asset is fundamentally strong, the investor has a long time horizon, and the purchase is part of a disciplined plan. It often fails when people treat every price drop as a sale, ignore why the price is falling, or use money they may need soon. A dip is not always a discount. Sometimes it is a warning label wearing a sale sticker.

This article breaks down how buying the dip works, when it may make sense, where it can go wrong, and why many long-term investors may be better served by dollar-cost averaging, diversification, and boring-but-beautiful patience.

What Does “Buy the Dip” Mean?

To buy the dip means purchasing an investment after its price has fallen from a recent high. For example, if a stock drops from $100 to $85, a dip buyer may see that 15% decline as an opportunity to buy shares at a lower price. The hope is that the price will recover and eventually move higher.

The strategy is built on one very old investing idea: buy low, sell high. Nobody argues with that phrase because it sounds perfect. The trouble is that real markets do not politely announce, “Hello, this is the low.” Instead, they drop, bounce, drop again, fake everyone out, rally at lunchtime, and then ruin someone’s spreadsheet by 3:59 p.m.

Buying the dip can apply to individual stocks, index funds, sector ETFs, cryptocurrency, bonds, or even real estate investment trusts. But the risk level changes dramatically depending on what you are buying. Buying a broad-market index fund after a market correction is very different from buying a collapsing company whose business model is quietly being eaten by competitors.

Why Investors Love Buying the Dip

The appeal is obvious. Everyone likes a bargain. If you would celebrate getting a laptop, sneakers, or a family-sized bag of tortilla chips at 20% off, why not feel the same about a stock?

There are several reasons the strategy attracts investors:

1. Lower prices can improve future returns

If you buy a quality asset at a lower price and it later recovers, your return can be stronger than if you had bought at the top. This is the math that makes dip buying attractive. A stock that falls from $100 to $80 only needs to rise $20 to return to its old price, but that $20 gain represents a 25% return from the $80 purchase price.

2. Market declines are common

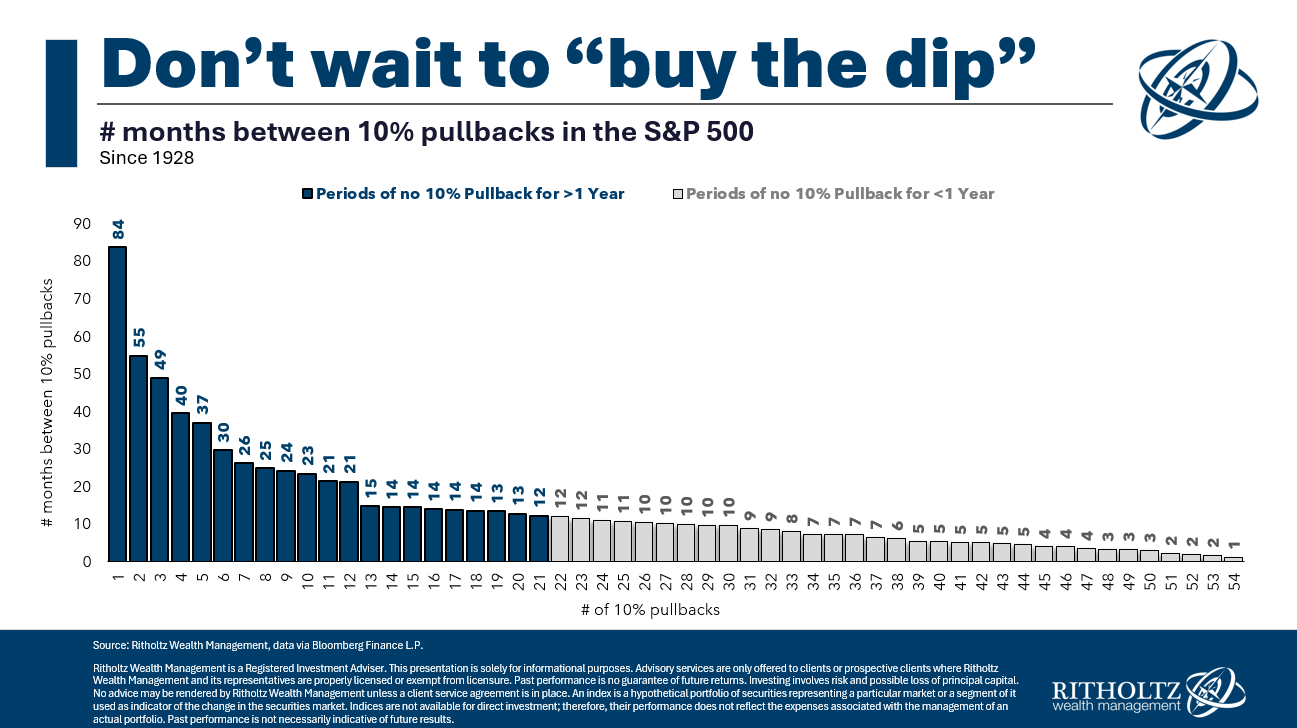

Pullbacks, corrections, and bear markets are part of investing. A pullback is often considered a decline of about 5% to 10%, a correction is commonly around 10% to 20%, and a bear market is usually a drop of 20% or more from a recent high. These declines can feel dramatic, but they are not rare. Long-term investors should expect the market to occasionally act like it stepped on a rake.

3. It feels proactive

Many investors hate doing nothing during volatility. Buying the dip gives them a sense of control. Instead of watching prices fall and whispering motivational quotes to their brokerage app, they are taking action. That emotional benefit can be real, but action is not always the same as wisdom.

Does Buy the Dip Actually Work?

Buying the dip can work under the right conditions. However, it is not magic. It is a strategy that depends on timing, asset quality, cash management, and emotional discipline. Remove any one of those ingredients and the recipe starts tasting like regret.

For broad market indexes, buying after large declines has often rewarded patient investors over long periods because the U.S. stock market has historically recovered from major downturns and gone on to reach new highs. That does not mean every decline recovers quickly. Some downturns take months. Others take years. Investors who buy too early may watch their “dip” become a deeper dip, then a canyon, then something that requires a flashlight and emotional support snacks.

For individual stocks, the answer is more complicated. A strong company can temporarily fall because of broad market fear, short-term earnings disappointment, rising interest rates, or investor overreaction. In those cases, buying the dip may be reasonable if the business remains healthy. But some stocks fall because the company’s future has genuinely worsened. Revenue may be shrinking, debt may be rising, margins may be collapsing, or competitors may be stealing market share. Buying that dip is not bargain hunting; it is volunteering to hold the bag.

Buy the Dip vs. Dollar-Cost Averaging

Dollar-cost averaging means investing a fixed amount at regular intervals, regardless of market conditions. For example, someone might invest $200 every month into an S&P 500 index fund. When prices are high, that money buys fewer shares. When prices are low, it buys more shares. No crystal ball required.

This is where buying the dip gets awkward. If you wait for dips, your cash may sit on the sidelines while the market keeps rising. That can hurt long-term returns because stocks have historically gone up more often than they have gone down over long periods. The best days in the market also tend to cluster near scary periods, which means investors who jump in and out can miss powerful rebounds.

Dollar-cost averaging does not guarantee profits or protect against losses, but it reduces the pressure to perfectly time the market. It also helps investors build a habit. And habits matter, because most portfolios are not destroyed by math. They are destroyed by panic, greed, overconfidence, and the mysterious human desire to sell low after buying high.

When Buying the Dip May Make Sense

Buying the dip is more likely to work when it is tied to a clear plan instead of a dramatic mood swing. Here are situations where the strategy may be reasonable.

The asset is diversified

Buying dips in a broad-market ETF or index fund is generally less risky than buying dips in one company. A diversified fund spreads risk across many businesses. One company can go bankrupt. The entire U.S. market going permanently to zero would require a much bigger problem than your brokerage balance.

The investor has a long time horizon

Buying a dip with money needed next month is risky. Markets can stay down longer than expected. Dip buying works best when the investor can wait through volatility and does not need to sell during a downturn.

The decline is caused by temporary fear

Sometimes good assets fall because investors are nervous about inflation, interest rates, elections, earnings season, or global events. If the long-term case remains intact, a lower price may create opportunity. The key question is not “Did it fall?” The key question is “Why did it fall?”

The investor uses a rule-based approach

A disciplined investor might decide in advance to invest extra money when a diversified fund falls 10%, 15%, or 20%. That is different from panic-scrolling financial news and buying whatever looks red enough to be “cheap.” Rules reduce emotional decision-making.

When Buying the Dip Can Go Wrong

Buying the dip fails when investors confuse a lower price with a better value. Price and value are related, but they are not identical. A stock that falls 70% can still be expensive if the business is deteriorating fast enough.

You may catch a falling knife

The famous phrase “catching a falling knife” describes buying while an investment is still dropping hard. The first dip may not be the final dip. A stock down 20% can fall another 20%, and then another. Mathematically, a 50% loss requires a 100% gain just to break even. That is not a dip; that is a treadmill with accounting software.

You may run out of cash

Many dip buyers keep cash aside for “better prices.” That sounds smart until the market rises for years and the cash earns less than the investments they avoided. Or they buy the first dip aggressively, leaving no cash for a deeper decline. Good dip buying requires cash management, and cash management requires patience.

You may ignore opportunity cost

Waiting for a dip can mean missing gains. If a fund rises 30% while you wait for a 10% decline, you may still end up buying at a higher price than if you had invested earlier. This is one reason many long-term investors prefer steady contributions over waiting for the perfect entry.

You may underestimate your emotions

It is easy to say you will buy when the market crashes. It is harder when every headline sounds like the economy just tripped over a power cord. Many investors plan to buy dips, then freeze when the dip actually arrives. Others buy too early, panic, and sell before the recovery.

Specific Examples: The Good, the Bad, and the “Oops”

Imagine two investors: Alex and Jordan. Alex invests $500 every month into a diversified index fund. Jordan keeps cash aside and waits for a 15% market drop. If the market falls soon, Jordan may get a better entry price. But if the market rises for two years before dropping 15%, Jordan may buy at a price higher than where Alex started. Alex’s boring plan may beat Jordan’s dramatic strategy simply because the money was invested earlier.

Now consider an individual stock. Suppose a profitable technology company drops 12% after reporting slower growth, but it still has strong cash flow, loyal customers, low debt, and a durable competitive advantage. A dip buyer who has studied the business may see an opportunity.

But suppose another company drops 40% because its main product is losing demand, debt is expensive, insiders are leaving, and management says “temporary headwinds” seventeen times on the earnings call. That may not be a dip. That may be the market correctly lowering the price because the business is worth less.

A Smarter Way to Buy the Dip

If you want to use a buy-the-dip strategy, consider making it systematic. A plan beats vibes. Vibes are for playlists, not portfolios.

Step 1: Keep your emergency savings separate

Do not use rent money, tuition money, medical money, or emergency savings to buy dips. Investing should use money that can remain invested for years. A market bargain is not a bargain if it forces you to sell at a bad time because life happened.

Step 2: Define what counts as a dip

Decide in advance what decline matters. Is it 5%, 10%, 20%, or more? Without a definition, every red day can feel like an urgent invitation.

Step 3: Use position sizing

Instead of investing all available cash at once, divide it into portions. For example, an investor might deploy 25% of planned cash after a 10% decline, another 25% after 15%, and more after 20%. This approach does not guarantee success, but it reduces the risk of going all-in too early.

Step 4: Focus on quality

For individual stocks, review revenue trends, profits, debt, cash flow, competitive position, valuation, and management quality. For funds, understand what the fund owns, its fees, and how it fits your overall allocation.

Step 5: Know when you are wrong

Before buying, ask: What would change my mind? If the answer is “nothing,” that is not conviction. That is stubbornness wearing a blazer.

Buy the Dip and Long-Term Investing

For long-term investors, the best version of buying the dip may be simple: keep investing regularly, and if the market drops sharply, invest a little extra if your financial situation allows. This combines the discipline of dollar-cost averaging with the opportunistic benefit of lower prices.

In other words, do not build your entire strategy around waiting for dips. Make buying the dip a side dish, not the whole buffet. Your core plan may include diversified funds, regular contributions, a target asset allocation, periodic rebalancing, and a long time horizon. Dip buying can be added carefully, but it should not replace the foundation.

Does Buy the Dip Work for Beginners?

Beginners should be careful. Buying the dip sounds easy because the phrase is short. But the actual work involves understanding valuation, risk, diversification, business quality, taxes, time horizon, and personal cash needs. That is a lot to ask from a three-word slogan.

For newer investors, dollar-cost averaging into diversified funds may be easier and less stressful. It avoids the pressure of deciding whether today’s decline is a golden opportunity or the market clearing its throat before yelling louder tomorrow.

If beginners do try dip buying, they may want to do it with small amounts, avoid concentrated bets, and write down the reason for each purchase. Writing things down is powerful because it forces clarity. Also, future you can read it and say, “Wow, past me really thought a meme stock with no earnings was a retirement plan.”

Final Verdict: Does Buy the Dip Work?

Yes, buying the dip can work, but it is not a guaranteed shortcut to wealth. It works best when investors buy quality assets, stay diversified, use money they do not need soon, and follow a disciplined plan. It works poorly when investors chase falling stocks, ignore fundamentals, rely on emotion, or wait so long for a perfect dip that they miss years of market growth.

The biggest lesson is this: buying the dip is not automatically smarter than simply staying invested. For many people, the most reliable strategy is regular investing, diversification, patience, and occasional opportunistic buying when prices fall. That approach may not sound exciting, but neither does brushing your teeth, and look how useful that turned out to be.

Markets reward discipline more often than drama. If you want to buy the dip, bring a plan, not a panic button.

Personal Experiences and Practical Lessons About Buying the Dip

Many investors first discover “buy the dip” during a market sell-off. Everything turns red, social media becomes a financial thunderstorm, and suddenly everyone has an opinion. Some people shout that it is the opportunity of a lifetime. Others warn that the market is doomed. The beginner stands in the middle, holding a phone, wondering whether the correct move is to invest, hide, or take up gardening.

One common experience is buying too early. An investor sees a favorite ETF fall 7% and thinks, “Great, discount time.” They buy. Then it falls another 8%. Now the original “smart entry” looks less heroic. This does not always mean the decision was bad, especially if the investment is diversified and long term. But it teaches a useful lesson: dips can keep dipping. That is why using several smaller purchases can feel much better than trying to nail the exact bottom.

Another experience is waiting too long. Some investors keep cash ready for a crash, but the market refuses to cooperate. It drops 3%, then rebounds. Drops 5%, then rebounds. Meanwhile, the investor keeps waiting for the “real” dip. Years later, they realize the market has moved much higher, and the perfect entry never arrived. This is one of the most frustrating parts of market timing: being too careful can become its own risk.

There is also the emotional roller coaster. Buying during a dip sounds brave until you do it and immediately see another red day. Even a solid plan can feel uncomfortable when headlines are dramatic. This is where experience matters. Investors who have lived through volatility often learn that discomfort is normal. The goal is not to eliminate fear; it is to avoid letting fear drive every decision.

A practical lesson many investors learn is to separate “core investing” from “opportunistic investing.” The core plan might be automatic monthly contributions to diversified funds. The opportunistic plan might be extra buying during major market declines. This structure helps prevent the all-or-nothing mindset. You are not forced to choose between investing everything today and waiting forever. You can do both in a balanced way.

Another helpful habit is reviewing past decisions. After buying a dip, write down why you bought, what you expected, and what would prove the thesis wrong. Months later, compare reality with your reasoning. This turns investing into a learning process instead of a scoreboard for ego. Sometimes you will be right for the wrong reason. Sometimes you will be wrong despite a reasonable process. The point is to improve the process.

The biggest experience-based takeaway is that buying the dip is less about courage and more about preparation. Investors who already know their goals, risk tolerance, cash needs, and asset allocation are better equipped to act during downturns. Investors who make decisions only after prices fall often feel rushed and emotional.

So, does buy the dip work in real life? It can, but only when it is treated as a disciplined tactic, not a personality trait. The market does not hand out medals for confidence. It rewards patience, preparation, and the ability to stay rational while everyone else is yelling at a candlestick chart.