Diversification is often described as the closest thing investing has to a seat belt. It will not prevent the crash, it will not make the road perfectly smooth, and it definitely will not stop investors from making dramatic faces at their brokerage app. But it can reduce the odds that one bad decision, one collapsing sector, or one “can’t-miss” stock turns a financial plan into confetti.

Still, every smart investor eventually asks the uncomfortable question: what is the worst case scenario for diversified portfolios? The honest answer is not “nothing bad can happen.” A diversified portfolio can lose money, sometimes a lot of it. In rare market environments, stocks, bonds, real estate, commodities, and even some alternative investments can fall together. The safety net can sag. The umbrella can leak. The portfolio that looked elegant in a spreadsheet can suddenly behave like a group chat during a power outage.

The real purpose of diversification is not to make losses disappear. It is to make losses more survivable. A well-diversified investment portfolio spreads risk across asset classes, sectors, regions, company sizes, and time horizons. When one part struggles, another may hold up better. But in a true worst case scenario, the usual offsets do not work as expected, correlations rise, liquidity dries up, inflation eats purchasing power, and investor behavior becomes the biggest risk of all.

This guide breaks down the dark side of diversified portfolios in plain English: what can go wrong, why it happens, how bad it can feel, and what investors can do before the storm arrives.

What Is a Diversified Portfolio?

A diversified portfolio is an investment mix designed to avoid relying on a single asset, company, sector, or economic outcome. Instead of putting all your money into one stock, one index, one country, or one theme, diversification spreads exposure across multiple sources of return.

A basic diversified portfolio might include U.S. stocks, international stocks, bonds, cash, and possibly real assets such as real estate investment trusts, commodities, or inflation-protected securities. A more advanced portfolio may include small-cap stocks, value stocks, emerging markets, short-term bonds, Treasury bonds, corporate bonds, gold, private assets, or alternative strategies.

The key idea is simple: investments do not all respond the same way to the same news. A recession may hurt stocks but help high-quality bonds. Inflation may pressure long-term bonds but support commodities or inflation-linked assets. A strong U.S. dollar may hurt international returns for American investors, while a weaker dollar may help them. Diversification is the art of not needing one perfect forecast to survive.

The Worst Case Scenario: Everything Falls Together

The nightmare version of diversification is a market environment where assets that are supposed to behave differently suddenly move in the same direction: down. Stocks fall because earnings expectations weaken. Bonds fall because interest rates rise. Real estate struggles because financing costs jump. International stocks decline because global growth slows. Commodities swing wildly. Cash feels safe but loses buying power to inflation.

This is the “no place to hide” scenario. It does not mean every asset loses the same amount, but it does mean the portfolio’s protective layers become thinner than expected. Investors who believed bonds would always cushion stock losses can be especially surprised when both decline together.

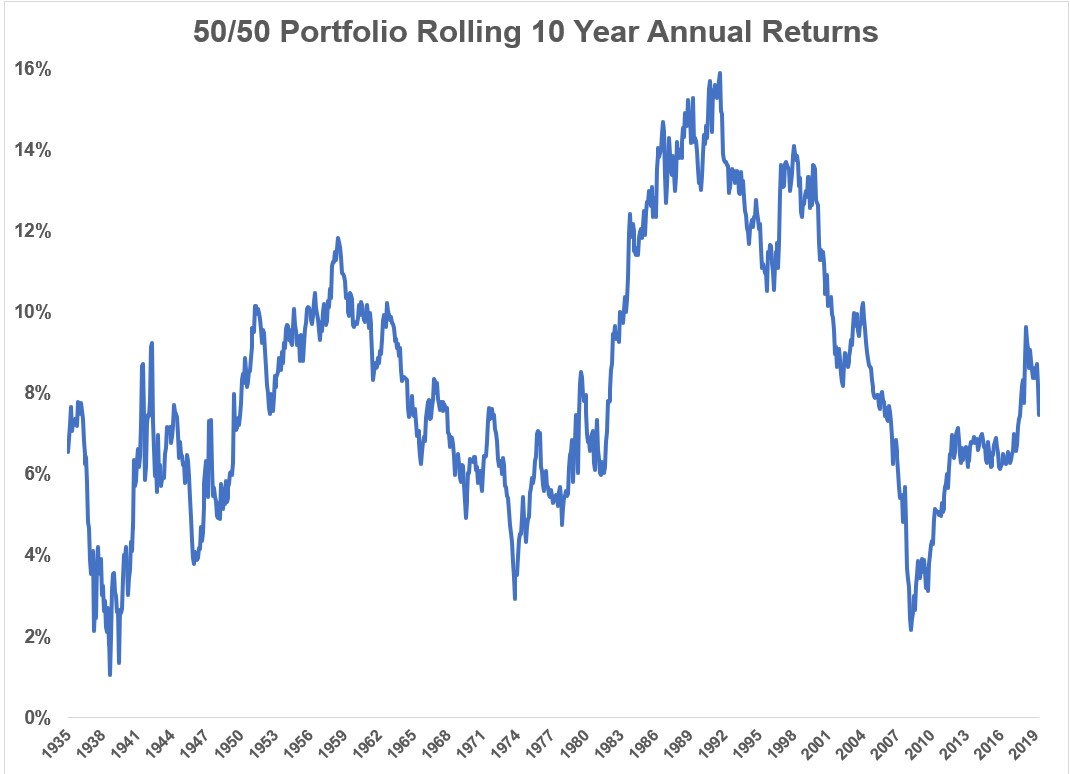

The classic example is the trouble experienced by balanced portfolios during inflationary shocks. When inflation rises quickly and central banks raise interest rates, stock valuations can compress while bond prices fall. That combination can be painful for a traditional 60/40 portfolio, which typically holds 60% stocks and 40% bonds. The portfolio is still diversified, but the two main engines are coughing at the same time.

Why Diversification Can Fail Temporarily

1. Correlations Rise During Market Stress

Correlation measures how investments move in relation to each other. In normal times, different assets often dance to different songs. During panic, they may all hear the same fire alarm. Investors sell what they can, not always what they want to. That can push many assets down together.

For example, stocks from different countries may look diversified on paper, but global markets are connected through trade, currencies, supply chains, investor flows, and central bank policy. When fear spreads, international diversification may reduce risk, but it may not fully protect against losses.

2. Inflation Attacks Both Stocks and Bonds

Inflation is one of the most dangerous enemies of diversified portfolios because it can pressure multiple assets at once. Rising inflation can reduce consumer purchasing power, increase business costs, and force central banks to raise interest rates. Higher rates often reduce the present value of future corporate earnings, which can hurt stocks. At the same time, rising rates push existing bond prices lower.

This is why inflationary bear markets can feel especially unfair. The investor thinks, “Fine, stocks are down, at least my bonds will help.” Then the bonds look back and say, “Actually, I’m busy falling too.” Rude? Yes. Historically possible? Also yes.

3. Liquidity Can Disappear

Liquidity means the ability to buy or sell an investment quickly at a fair price. In a crisis, liquidity can shrink. Certain bond funds, real estate funds, private assets, and niche investments may become harder to sell without accepting a discount.

This creates a hidden risk. An investor may own a diversified portfolio but still run into trouble if they need cash at the wrong time. A portfolio can be diversified and still illiquid. That is like owning five umbrellas locked in a car during a rainstorm.

4. Concentration Hides Inside “Diversified” Funds

Some investors believe they are diversified because they own a broad index fund. Often, they are more diversified than someone holding only a few individual stocks. But broad indexes can still become concentrated when a small group of large companies dominates market value.

If a handful of mega-cap stocks drive most of the index’s gains, the portfolio may become more exposed to one sector or theme than the investor realizes. The fund may hold hundreds of companies, but the largest names can still carry a lot of influence. Diversification by number of holdings is not the same as diversification by risk.

5. Investor Behavior Turns Losses Into Damage

The worst case scenario is not just a bad market. It is a bad market plus bad decisions. Selling after a large decline, abandoning a long-term strategy, chasing whatever just performed well, or moving entirely to cash after losses can turn a temporary drawdown into permanent damage.

Markets do not need investors to be perfect. But they do punish panic with impressive efficiency. A diversified portfolio can recover over time, but only if the investor stays invested in a plan that still makes sense.

How Bad Can a Diversified Portfolio Get?

The answer depends on the portfolio. A conservative portfolio with more cash and short-term bonds may decline less during a stock crash but may struggle to outpace inflation over long periods. An aggressive portfolio with mostly stocks may deliver higher long-term returns but can suffer deep drawdowns. A balanced portfolio sits in the middle, but “middle” does not mean painless.

A diversified stock portfolio can still lose 30%, 40%, or more during severe bear markets. A balanced stock-and-bond portfolio may lose less, but it can still experience double-digit declines. If bonds and stocks fall together, the drawdown can feel shocking because the portfolio is losing money in places investors expected stability.

Worst case outcomes may also include long recovery periods. A portfolio may eventually bounce back, but “eventually” can be a very annoying word when tuition, retirement withdrawals, or a home purchase are scheduled for next year. This is why time horizon matters. Money needed soon should usually be invested differently from money intended for retirement decades away.

The 60/40 Portfolio: Hero, Villain, or Misunderstood Side Character?

The 60/40 portfolio has been one of the most famous diversified portfolio models for decades. It combines growth from stocks with stability and income from bonds. In many market environments, this mix has helped investors participate in stock market gains while reducing volatility compared with an all-stock portfolio.

But the 60/40 portfolio is not magic. Its worst case scenario appears when stock and bond returns are both pressured by the same force, especially unexpected inflation and rising interest rates. When that happens, bonds may not provide the usual cushion.

Does that mean the 60/40 portfolio is dead? Not necessarily. It means investors should understand what job each asset is supposed to do. Bonds can still provide income, reduce long-term volatility, and help during recessionary environments. But long-duration bonds can be vulnerable when rates rise sharply. A diversified bond allocation may need to include short-term bonds, high-quality bonds, Treasury Inflation-Protected Securities, or other fixed-income tools depending on goals and risk tolerance.

Worst Case Scenario by Investor Type

For Young Investors

Young investors usually have time on their side. Their worst case scenario is often not a temporary market crash, but panic-selling early and missing the recovery. A 25-year-old with decades until retirement may be able to withstand volatility if they have an emergency fund, stable income, and a sensible asset allocation.

The bigger risk is treating a diversified portfolio like a slot machine. Constantly changing strategies, chasing hot funds, or copying social media investing trends can destroy the benefits of diversification. A young investor does not need the perfect portfolio. They need a durable one.

For Pre-Retirees

Investors within 5 to 10 years of retirement face a more serious worst case: a major market decline right before withdrawals begin. This is called sequence-of-returns risk. The order of returns matters because withdrawing from a falling portfolio can lock in losses and reduce the money available for future growth.

For pre-retirees, diversification should not only focus on growth. It should also include cash reserves, high-quality bonds, flexible spending plans, and realistic retirement timelines. The goal is not to avoid every downturn. The goal is to avoid being forced to sell growth assets at terrible prices.

For Retirees

Retirees face a double threat: market declines and inflation. A portfolio that is too aggressive may suffer large drawdowns. A portfolio that is too conservative may fail to keep up with rising living costs. The worst case is needing portfolio income during a long market slump while inflation raises expenses.

This is why retirement diversification often requires different buckets: near-term cash, stable income assets, and long-term growth investments. The exact mix depends on spending needs, pensions, Social Security, healthcare costs, tax situation, and risk tolerance.

What Diversification Cannot Protect You From

Diversification is powerful, but it has limits. It cannot protect against every loss. It cannot remove market risk. It cannot guarantee income. It cannot make an unrealistic savings rate work. It cannot turn a short time horizon into a long one. It cannot fix high fees, emotional trading, poor tax planning, or unrealistic expectations.

Most importantly, diversification cannot protect investors from not understanding what they own. A portfolio filled with complicated funds, overlapping holdings, and trendy alternatives may look sophisticated but behave unpredictably. Complexity is not the same as safety. Sometimes it is just confusion wearing a nice jacket.

How to Prepare for the Worst Case Scenario

Build Around Goals, Not Headlines

A strong portfolio starts with the investor’s goals. Retirement in 30 years, a house down payment in three years, and emergency savings for next month should not be invested the same way. The shorter the timeline, the more important stability and liquidity become.

Keep Enough Cash for Real Life

Cash is not exciting. It will not impress anyone at dinner. But cash can prevent forced selling during a downturn. An emergency fund gives investors breathing room when markets are down, jobs are uncertain, or unexpected expenses show up with the subtlety of a marching band.

Diversify Within Asset Classes

Owning stocks and bonds is a start, but investors should also diversify within those categories. Stock exposure may include U.S. large-cap, small-cap, international developed, and emerging markets. Bond exposure may include short-term, intermediate-term, Treasury, investment-grade corporate, and inflation-linked bonds.

Watch Fees and Taxes

Fees are one of the few investment variables investors can control. High costs can quietly weaken returns over time. Taxes also matter, especially for taxable accounts. Asset location, tax-loss harvesting, and holding-period awareness can improve after-tax outcomes without requiring heroic market predictions.

Rebalance Before Emotions Take the Wheel

Rebalancing means bringing the portfolio back to its target allocation. If stocks rise sharply, rebalancing may involve trimming stocks and adding to bonds. If stocks fall, it may involve buying stocks when they feel emotionally radioactive. That is the point. Rebalancing turns discipline into a process instead of a mood.

Stress-Test the Portfolio

Investors should ask uncomfortable questions before markets do it for them. What happens if stocks fall 35%? What if bonds decline at the same time? What if inflation stays high? What if income drops? What if retirement starts during a bear market? Stress-testing does not predict the future, but it reveals whether the current plan is built for reality or just sunny weather.

Specific Example: The “Looks Safe” Portfolio That Wasn’t

Imagine an investor named Rachel. She owns 60% U.S. stocks and 40% long-term bonds. She considers the portfolio conservative because bonds make up a large portion. For several years, the mix works well. Stocks rise, bonds provide stability, and Rachel feels like a portfolio genius. She may even use the phrase “risk-adjusted returns” at brunch, which is legally allowed but socially risky.

Then inflation rises faster than expected. Interest rates climb. Stock valuations fall. Long-term bonds decline because their older, lower yields are less attractive than new bonds with higher yields. Rachel’s diversified portfolio loses money on both sides.

The problem is not that diversification failed forever. The problem is that Rachel’s bond allocation had a specific vulnerability: interest-rate risk. A more resilient version might include shorter-duration bonds, Treasury Inflation-Protected Securities, some cash for near-term needs, and global stock exposure. The lesson is clear: diversification should be based on risk factors, not just labels.

Specific Example: The “All-in on Safe Cash” Mistake

Now imagine Marcus, who watched a market crash and moved his retirement savings almost entirely to cash. At first, he feels brilliant. His account stops bouncing around. But years pass, prices rise, and his money buys less. Meanwhile, markets recover, but Marcus waits for the “perfect” time to get back in. The perfect time, naturally, never sends a calendar invite.

Marcus avoided short-term volatility but accepted long-term purchasing power risk. This is one of the sneakiest worst case scenarios for conservative investors. The account balance may look stable, but real wealth declines after inflation. Diversification must protect against both market losses and the risk of being too safe for too long.

Experiences and Practical Lessons From Diversified Portfolio Downturns

Investors often learn the most about diversification when the portfolio is misbehaving. During calm markets, everyone likes to say they have a long-term mindset. During a downturn, that mindset gets tested by red numbers, scary headlines, and relatives asking whether “the market is going to zero.” Spoiler: relatives are rarely a reliable asset allocation tool.

One common experience is disappointment. Investors expect diversification to feel like protection, but in real life it often feels like losing less than the riskiest option. That is still valuable, but it is emotionally unsatisfying. If the stock market falls 35% and a diversified portfolio falls 18%, the investor may still feel terrible. The portfolio did its job, but the job was damage control, not mood enhancement.

Another experience is discovering hidden overlap. Many people own several funds and assume they are diversified because the account page looks busy. Then they realize most of the funds hold the same large U.S. technology companies. The portfolio has variety in names, but not necessarily variety in risk. A true review looks under the hood: sectors, regions, market capitalization, bond duration, credit quality, currency exposure, and fees.

Investors also learn that cash has emotional value. A cash reserve may drag on returns during bull markets, but it can be priceless during a bear market. Knowing that near-term expenses are covered can make it easier to leave long-term investments alone. This is not because cash is a superior growth asset. It is because cash protects decision-making. In a crisis, calm is an asset class too.

Another lesson is that rebalancing feels backwards. Buying more stocks after a decline can feel like walking into a store where everything is on sale and wondering if the store is haunted. Yet systematic rebalancing is one of the clearest ways to maintain discipline. It forces investors to sell some of what has become expensive and buy some of what has become cheaper, based on a plan created before emotions took over.

Many investors also discover that risk tolerance is not theoretical. A questionnaire may say someone can handle a 25% decline. Reality may say otherwise at 2:17 a.m. when they are scrolling market news under a blanket. The best portfolio is not always the one with the highest expected return. It is the one the investor can actually hold through ugly markets without blowing it up at the worst moment.

Finally, downturns teach humility. No portfolio is invincible. No allocation works in every environment. No expert knows the future with perfect accuracy. Diversification is not a promise that nothing bad will happen. It is a recognition that many different bad things can happen, and investors should not bet their entire future on guessing which one arrives next.

Conclusion: The Worst Case Is Bad, But Not Unmanageable

The worst case scenario for diversified portfolios is a period when multiple assets fall together, inflation reduces purchasing power, liquidity becomes scarce, and investor behavior turns temporary losses into permanent ones. That is the scary version. It can happen. It has happened in different forms before. It will probably happen again, because markets enjoy reminding humans that confidence and certainty are not the same thing.

But the conclusion is not that diversification is useless. The conclusion is that diversification must be thoughtful. A resilient portfolio considers asset allocation, time horizon, inflation risk, liquidity, fees, taxes, behavior, and the possibility that yesterday’s safe haven may not work perfectly tomorrow.

For most long-term investors, the goal is not to build a portfolio that never falls. That portfolio does not exist, unless it is imaginary, and imaginary portfolios have suspiciously excellent returns. The real goal is to build a portfolio that can bend without breaking, recover without requiring perfect timing, and support financial goals through more than one economic season.

Diversification is not a guarantee. It is a survival strategy. And in investing, survival is not boring. Survival is how compounding gets enough time to do its quiet, magnificent work.