Let’s begin with the line that makes finance TV producers sit up straighter in their very expensive chairs: yes, the stock market is going to crash. Absolutely. One day, it will tumble hard, experts will look shocked on camera, social media will become a digital panic room, and somebody’s uncle will announce that he “saw it coming” right after it happened.

Now for the part that matters: nobody knows exactly when.

That distinction is the whole game. Saying the market will crash eventually is not a bold prophecy. It is closer to saying winter will return, traffic will be annoying, and your favorite stock guru will eventually post a thread that ages like warm milk. Market crashes are not glitches in the system. They are part of the system. They happen because markets are made of human beings, and human beings are brilliant, emotional, greedy, fearful, imaginative, and occasionally allergic to patience.

So if the title sounds dramatic, good. It should. But the point of this article is not to sell panic. It is to explain why crashes are inevitable, what usually causes them, why most people respond badly, and what smart investors do when the market decides to cosplay as a trapdoor.

Why a Stock Market Crash Is Inevitable

Markets move in cycles. They rise, cool off, recover, stretch, wobble, and sometimes fall out of bed. That is true whether the trigger is a speculative bubble, a recession, aggressive interest-rate hikes, a banking scare, geopolitical stress, or a sudden realization that investors were paying heroic prices for very ordinary profits.

The stock market does not travel upward in a straight line because the economy does not move in a straight line. Corporate earnings expand and contract. Credit gets easier and then tighter. Consumers spend more freely and then get cautious. Investors become optimistic, then euphoric, then unreasonable, then terrified. In other words, Wall Street is not powered only by spreadsheets. It is powered by mood swings wearing loafers.

Crashes happen when expectations outrun reality by too much. Prices rise on the assumption that growth will remain strong, rates will stay friendly, liquidity will keep flowing, and buyers will keep paying more tomorrow than they did today. That works beautifully until it doesn’t. Once that confidence cracks, prices can fall much faster than they rose, because panic is usually more efficient than optimism.

That is why the statement “the stock market is going to crash” is both true and incomplete. The market always carries crash risk. What changes is the setup, the severity, and the timeline.

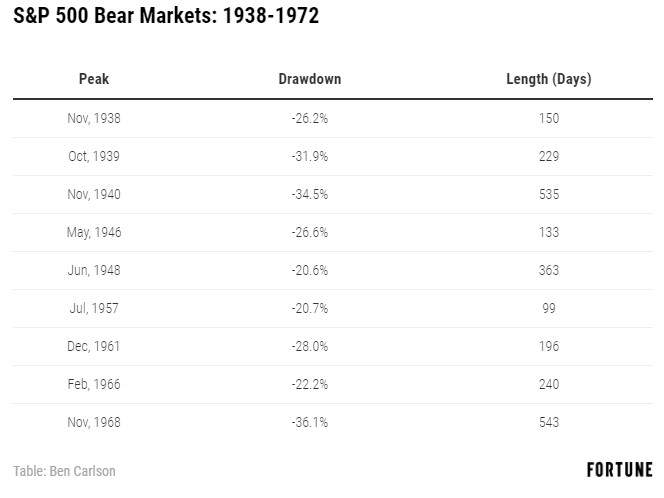

Crash, Correction, and Bear Market: Not the Same Beast

One reason stock-market headlines are so messy is that people use several terms as if they mean the same thing. They do not.

Market correction

A correction usually means a meaningful pullback, often around 10% from a recent high. Corrections are common. They are unpleasant, but they are not automatically disasters. Many are simply the market’s way of reminding everyone that stocks are not savings accounts with better branding.

Bear market

A bear market is generally a drop of 20% or more from a recent high. Bear markets tend to feel different because they are not just about falling prices. They come with collapsing confidence, louder recession talk, and a growing urge among investors to “do something” right before doing the worst possible thing.

Crash

A crash is less about a neat percentage label and more about speed, violence, and psychology. A crash is when prices fall so fast that the decline feels chaotic. It is when “long-term perspective” suddenly sounds less like wisdom and more like a dare.

In practice, a crash can become part of a bear market, or it can be a short, brutal episode inside a broader recovery. The important point for readers is this: not every dip becomes a collapse, but every major collapse begins with weakness that many people initially dismiss.

What Usually Causes a Stock Market Crash?

There is no single master switch labeled Crash Now. Most major downturns come from a combination of stress factors that build quietly, then break all at once.

1. Overvaluation

When stock prices climb much faster than profits, the market becomes more fragile. Investors can tolerate expensive stocks for a while, especially when excitement is high and money is easy. But rich valuations leave little room for disappointment. When growth slows even slightly, expensive stocks can reprice with shocking speed.

2. Tight financial conditions

Higher interest rates make borrowing costlier, reduce the appeal of risk assets, and pressure corporate valuations. The higher the rate environment, the less investors are usually willing to pay for future earnings. That is especially painful for highly valued growth stocks and businesses built on “trust us, profits are coming later.”

3. Recession fears

When investors believe the economy is weakening, they start cutting expectations for earnings, hiring, and consumer demand. Sometimes the market falls before a recession officially arrives. Other times it falls without one. The market is a forward-looking machine, which is a fancy way of saying it loves to panic about tomorrow before tomorrow has even clocked in.

4. Excess leverage

Borrowed money makes bull markets feel smarter and crashes feel meaner. Leverage forces selling. Margin calls do not care about your long-term thesis, your motivational quotes, or the fact that you “still believe in the company.” They want cash.

5. A catalyst nobody expected to matter that much

Sometimes it is a bank failure. Sometimes a policy mistake. Sometimes a global shock. Sometimes it is simply the moment investors realize the story they were buying has become too fragile to survive scrutiny. Markets often look stable right up until they do not.

History’s Favorite Plot Twist: “This Time Is Different”

Before major selloffs, markets often produce the same comforting phrase: this time is different. It appears in every era wearing different clothes.

In 1929, investors believed a new age of prosperity had arrived. In the dot-com era, many acted as if profits were optional as long as a company had a futuristic name and a website. Before the 2008 financial crisis, plenty of people treated housing and credit as if they had become permanently safer. In 2020, panic arrived at lightning speed for an entirely different reason, proving once again that the market does not need to repeat the same script to deliver the same emotional damage.

The lesson is not that growth stories are fake or that innovation is dangerous. The lesson is that when investors stop respecting risk, risk usually reintroduces itself with a folding chair.

So Is the Market About to Crash Right Now?

That is the million-dollar question, and also the question most likely to make honest analysts sigh into their coffee.

The responsible answer is this: maybe, eventually, but no one can give you a reliable date. Markets can stay expensive longer than critics expect. They can shrug off weak news, rally through uncertainty, and continue climbing while bearish headlines pile up like unopened bills. They can also reverse suddenly when confidence, liquidity, or earnings expectations crack.

In other words, the title of this article is true in the long run but dangerous in the short run if people interpret it as a countdown clock. Predicting that a crash will happen someday is easy. Predicting next month’s close is how people end up inventing fresh excuses in public.

That is why serious investors do not build their entire strategy around apocalypse forecasting. They build around resilience.

What Smart Investors Do Instead of Playing Fortune Teller

Build a portfolio that can survive bad years

Diversification is not exciting. It will never trend on social media. It does not make people feel like geniuses at dinner parties. But it remains one of the simplest ways to reduce risk. Spreading exposure across different asset types, sectors, and time horizons can help soften the blow when one part of the market gets hit harder than the rest.

Match risk to reality

Lots of investors say they can handle volatility right up until volatility introduces itself properly. A good portfolio is not the one that looks heroic in a bull market. It is the one you can actually hold when headlines scream, portfolios bleed, and everybody online suddenly becomes a macroeconomist.

Keep cash for life, not for drama

An emergency fund is not just a budgeting tool. It is an anti-panic device. Investors are more likely to sell at terrible moments when they also need money for rent, medical bills, tuition, or a surprise expense that arrived with the timing of a movie villain.

Rebalance instead of reacting

Rebalancing imposes discipline. It forces investors to trim what has run too far and add to what has become underweight. That feels boring, which is precisely why it can be effective. Markets often punish emotion and reward process.

Respect complicated products

Many people assume all exchange-traded products are simple because they trade like stocks. Not true. Some leveraged and inverse products behave very differently from what casual investors expect, especially over longer holding periods. When markets get rough, complexity can become gasoline.

The Biggest Mistakes People Make During a Crash

Selling everything after the damage is already done

This is the classic move. Prices fall, fear rises, and investors sell not because their plan changed but because their emotions did. The trouble is that the market’s strongest recovery days often show up near its ugliest moments. Miss those days and long-term returns can suffer badly.

Believing one indicator is magic

Yield curves, valuations, credit spreads, unemployment trends, sentiment surveys, and earnings revisions all matter. None of them is a crystal ball. Investors get into trouble when they fall in love with a single signal and ignore the broader picture.

Using too much leverage

Leverage is like hot sauce: a little can change the flavor, too much can ruin your whole evening. Borrowing amplifies gains on the way up and pain on the way down. In a fast selloff, it can turn a manageable drawdown into forced liquidation.

Confusing activity with skill

During turbulent markets, constant action feels productive. It is often just stress in a necktie. Refreshing charts every six minutes is not a strategy. It is cardio for your thumb.

What a Realistic Investor Mindset Looks Like

A realistic investor does not say, “Crashes will never happen.” A realistic investor says, “Crashes are part of owning risk assets, so I will prepare before one arrives.”

That mindset matters because it shifts the question from prediction to preparation.

Instead of asking whether the market will crash, ask:

- Would my portfolio still make sense if stocks dropped hard?

- Do I have enough cash to avoid panic selling?

- Am I diversified, or just accidentally concentrated?

- Do I own investments I actually understand?

- Am I investing according to a plan, or according to vibes?

Those questions are less dramatic than a market-crash headline. They are also far more useful.

Conclusion

Yes, the stock market is going to crash. Not because the financial world is broken beyond repair, and not because every gloomy forecast deserves applause, but because crashes are a normal feature of markets built on risk, growth, uncertainty, and human behavior.

The mistake is not accepting that crashes will happen. The mistake is thinking that certainty about eventual crashes somehow gives anyone certainty about immediate timing.

That is where investors get wrecked. They hear “a crash will come” and translate it into “I should abandon my plan today.” But history suggests a better lesson: respect risk, stay diversified, avoid panic, keep enough liquidity, and do not mistake fear for foresight.

The market will crash again. One day, the headlines will howl, commentators will point at charts like weather forecasters tracking a tornado, and social media will fill with declarations that civilization has entered its flop era. When that day comes, the people best positioned to survive will not be the loudest prophets. They will be the investors who planned for turbulence before the sky got weird.

What the Experience of a Crash Actually Feels Like

If you have never lived through a serious selloff, it is easy to imagine a crash as a clean, cinematic event: one giant red day, a dramatic headline, a villain, a lesson, roll credits. Real life is messier. A crash often feels like a slow leak, then a punch in the face, then a strange period where every day seems to begin with hope and end with somebody throwing a chair.

At first, investors usually minimize it. They call it a healthy pullback, a buying opportunity, a temporary overreaction, a chance to shake out weak hands. That language can be reasonable in the early stages. The problem is that the same phrases get repeated even when conditions have clearly worsened. People do not like updating their beliefs when money is involved.

Then comes the emotional middle stage, and this is where the experience becomes deeply personal. You open your account more often even though it never improves your mood. You start reading more headlines, not fewer, despite the fact that most of them are just fear wearing better punctuation. You suddenly remember every reckless decision you ever made with money. Stocks you once planned to hold for years start looking suspicious by lunchtime.

Experienced investors are not immune to this. They just recognize the pattern faster. They know the temptation to “wait until things calm down” often means selling low and buying back higher. They know that a crash does not merely test portfolios; it tests identity. It asks whether your investment plan was a real plan or just a confident speech you gave yourself in easier times.

There is also a strange social element. During a major downturn, everyone becomes more certain in public and less certain in private. The permabears act triumphant. The permabulls become philosophers. Your group chats turn into mini economic councils filled with strong opinions and almost no accountability. Someone insists cash is king. Someone else announces that this is the opportunity of a lifetime. Usually, both are speaking too absolutely.

And yet, hidden inside that discomfort is something useful. Crashes force clarity. They reveal whether you were overexposed, overleveraged, underprepared, or simply overconfident. They expose weak assumptions. They also teach patience in a way bull markets never can. A rising market makes almost everybody feel clever. A falling market separates discipline from theater.

Most people who live through a real crash remember less about the chart and more about the feeling: the nausea, the second-guessing, the relief rallies that fizzle, the weird calm that eventually returns, and the surprise of realizing that markets, businesses, and daily life do in fact continue. That may be the most important experience-related lesson of all. A crash feels like the end while you are inside it. In hindsight, it is usually a brutal chapter, not the whole story.