How much has PolicyGenius raised in funding? The clean answer is: Policygenius has raised more than $276 million in publicly reported funding, with some funding databases placing the total closer to the high-$280 million range depending on how they classify rounds, debt facilities, and later financing details. The company itself announced in March 2022 that its $125 million Series E brought total funding to “more than $250 million,” while investor databases and finance publishers commonly cite totals above $276 million.

That may sound like a number pulled from a Silicon Valley bingo machine, but the story behind it is actually useful. Policygenius did not raise money just because “insurtech” sounded fancy on a pitch deck. The company raised capital because it was trying to solve a very real consumer problem: buying insurance is often confusing, slow, paperwork-heavy, and about as fun as assembling furniture without instructions.

Founded in 2014 by Jennifer Fitzgerald and Francois de Lame, Policygenius built an online insurance marketplace where consumers could compare life insurance, disability insurance, renters insurance, homeowners insurance, auto insurance, and other financial protection products. Instead of making people call five agents, decode policy language, and guess whether they were underinsured, Policygenius positioned itself as a simpler digital front door for insurance shopping.

Policygenius Funding at a Glance

Policygenius raised capital across multiple rounds, from an early seed round to a large Series E. The broad funding path looks like this:

| Round | Approximate Date | Reported Amount | Notable Investors |

|---|---|---|---|

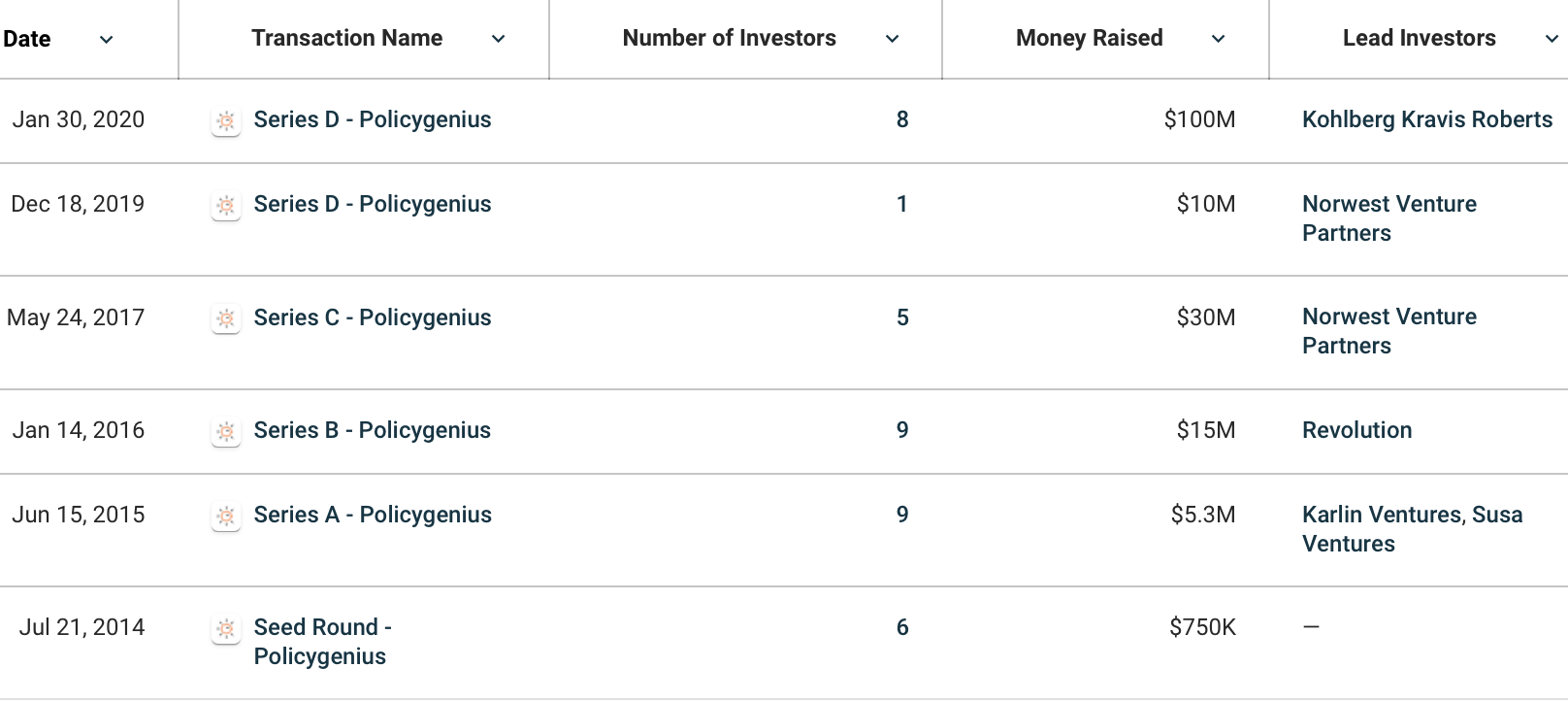

| Seed | 2014 | About $750,000 | Early angel and venture investors |

| Series A | 2015 | About $5.3 million | Susa Ventures, Karlin Ventures, AXA Strategic Ventures, Transamerica Ventures |

| Series B | 2016 | $15 million | Revolution Ventures, Susa Ventures, Karlin Ventures, MassMutual Ventures, Transamerica Ventures |

| Series C | 2017 | $30 million | Norwest Venture Partners, Revolution Ventures, AXA Strategic Ventures, MassMutual Ventures |

| Series D | 2020 | $100 million | KKR, Norwest Venture Partners, Revolution Ventures, Susa Ventures, AXA Venture Partners |

| Series E | 2022 | $125 million | KKR, Norwest Venture Partners, Revolution Ventures, Brighthouse Financial, Global Atlantic, Lincoln Financial, Pacific Life, MassMutual Ventures |

Add those major public rounds together, and the answer lands above $276 million. Depending on the source, the number may appear as roughly $276 million, $287 million, or $288 million. The difference usually comes from whether smaller financing, debt facilities, or data-provider adjustments are included. For readers who want a practical answer, “over $276 million” is the safest public figure.

Why Did Policygenius Raise So Much Money?

Insurance is a massive market, but massive does not always mean modern. For decades, the consumer insurance experience relied on local agents, manual underwriting, phone calls, PDFs, and a surprising number of forms that looked like they were designed during the fax-machine golden age.

Policygenius entered the market with a simple promise: help people compare policies online, get advice, and buy coverage without needing a decoder ring. That sounds obvious now, but in the early 2010s, insurance was still behind banking, investing, travel, and shopping in consumer-facing digital convenience.

The First Big Bet: Insurance Comparison

The original value proposition was comparison. Consumers could compare quotes from multiple insurance companies rather than relying on a single provider’s offer. That matters because life insurance pricing can vary widely by age, health, coverage amount, term length, and underwriting class. Two people can ask for the same $1 million policy and receive very different offers based on individual risk factors.

Policygenius gave shoppers a way to see options side by side. In personal finance, that kind of transparency is powerful. It is the same reason people compare mortgage rates, credit cards, brokerage fees, and high-yield savings accounts. When the product is expensive and long-term, a better comparison process can save real money.

The Second Big Bet: Human Help Plus Software

Policygenius was not purely a “click three buttons and buy” platform. Insurance is regulated, emotional, and filled with edge cases. A parent buying life insurance may have questions about beneficiaries, medical exams, laddering policies, term length, or whether employer coverage is enough. A homeowner may need help understanding replacement cost, deductibles, exclusions, and bundling.

That is why Policygenius combined digital tools with licensed experts. This hybrid model required capital. Hiring licensed agents, building carrier integrations, maintaining compliance, and improving underwriting workflows are not cheap. In other words, Policygenius was not just building a pretty website; it was building infrastructure in a heavily regulated industry.

Breaking Down the Major Funding Rounds

Seed and Series A: Proving the Concept

The early rounds helped Policygenius prove that consumers were willing to shop for insurance online. This stage was about product-market fit: could a digital marketplace make insurance feel less intimidating? Could consumers trust an online platform with serious financial decisions? Could carriers see enough value to partner with a startup?

The early answer was yes. The company’s initial capital helped it build its platform, grow its team, and expand beyond a narrow insurance category. Early investors were betting that insurance distribution would eventually look more like other digital marketplaces.

Series B: Expanding the Marketplace

The $15 million Series B in 2016 gave Policygenius more fuel to broaden its product lines and customer reach. The company was no longer just proving that online insurance comparison could work. It was trying to become a recognized consumer brand in financial protection.

At this stage, investors saw the opportunity to modernize a large but clunky market. Life insurance, disability insurance, renters insurance, and pet insurance all had consumer pain points. Policygenius could use content, calculators, quote tools, and licensed support to guide people through decisions they often postponed.

Series C: Scaling With Norwest

In 2017, Policygenius raised $30 million in Series C funding led by Norwest Venture Partners. This was a major credibility moment. The company had moved from “interesting startup” to “serious insurtech platform.”

The Series C helped Policygenius expand its consumer insurance platform, hire across the organization, and deepen partnerships. By this point, the company had already helped many shoppers compare life insurance coverage and was becoming better known in the broader personal finance ecosystem.

For a startup, this stage is like moving from a food truck to a restaurant. The recipe may work, but now you need operations, staff, systems, quality control, and enough cash to avoid turning the kitchen into a fire drill.

Series D: The $100 Million KKR Round

The 2020 Series D was the big leap. Policygenius announced $100 million in funding led by KKR, with participation from existing investors including Norwest Venture Partners, Revolution Ventures, Susa Ventures, AXA Venture Partners, MassMutual Ventures, and Transamerica Ventures.

This round signaled that large institutional investors believed Policygenius could become a major player in digital insurance distribution. The company said it had grown annualized revenue significantly since its Series C and planned to use the capital for hiring and broader financial protection products.

The timing was also important. In 2020, the COVID-19 pandemic accelerated consumer interest in life insurance while also making traditional medical exams and in-person processes harder. Digital underwriting, no-exam life insurance, and online insurance shopping became more relevant almost overnight.

Series E: The $125 Million Growth Round

In March 2022, Policygenius raised $125 million in Series E growth capital. The round included existing investors such as KKR, Norwest Venture Partners, and Revolution Ventures, as well as major insurance industry names including Brighthouse Financial, Global Atlantic Financial Group, iA Financial Group, Lincoln Financial, Pacific Life, AXA Venture Partners, and MassMutual Ventures.

This was not just venture money chasing growth. The presence of major life insurance and annuity carriers suggested strategic interest from the industry itself. Carriers wanted better distribution. Consumers wanted simpler shopping. Policygenius sat in the middle, trying to make both sides less frustrated.

Policygenius also secured a credit facility from ORIX Growth Capital and refinanced an existing senior loan facility with JPMorgan Chase. That detail matters because later-stage startups often use both equity and debt-like financing to support growth, manage cash flow, or fund operations without giving up as much ownership.

So Why Do Funding Totals Differ?

If one source says Policygenius raised over $276 million and another says around $287 million, is somebody wrong? Not necessarily. Funding databases often categorize financing differently. One may count only equity rounds. Another may include certain debt facilities. A third may update figures based on private filings, secondary sources, or investor disclosures.

The most conservative public-company-announcement figure after the Series E is “more than $250 million.” The commonly cited media and database figure is “over $276 million.” Some financial databases place the total closer to $287 million or $288 million. For an article written for general readers, the best explanation is this: Policygenius raised at least $276 million in widely reported funding, with some sources estimating total financing near $288 million.

What Happened After the Funding?

Raising a lot of money does not automatically mean a startup cruises into a happy IPO. The insurtech market became more difficult after the pandemic-era funding boom. Public technology valuations fell, interest rates rose, venture investors became more cautious, and companies that once chased growth at all costs had to focus on efficiency.

Policygenius faced the same broader pressure as many late-stage startups. In 2023, Zinnia, an insurance technology and digital services company backed by Eldridge, announced it was acquiring Policygenius. The deal was designed to combine Policygenius’ digital marketplace and distribution strengths with Zinnia’s technology platform for life insurance and annuities.

The acquisition shifted the story. Policygenius was no longer simply a venture-backed company aiming for a standalone public-market future. It became part of a larger insurance technology platform. That does not erase the funding story; it completes an important chapter.

Was Policygenius a Success?

The answer depends on the measuring stick. From a consumer perspective, Policygenius helped normalize online insurance shopping. It made life insurance and other protection products easier to compare, easier to understand, and less intimidating for many households.

From a venture-capital perspective, the answer is more complicated. Policygenius raised hundreds of millions of dollars and attracted respected investors, but the eventual acquisition did not look like a classic high-flying IPO exit. Many late-stage startups from the 2020 and 2021 funding era experienced similar valuation pressure when public markets cooled.

Still, the company clearly influenced the insurance marketplace. It showed that consumers want transparency, digital convenience, and human guidance in one place. That combination remains relevant even as insurtech business models evolve.

What Investors Can Learn From Policygenius

Big Markets Attract Big Money

Insurance is enormous. Life insurance, property and casualty insurance, disability insurance, and annuities represent huge pools of premiums and commissions. Startups that can improve distribution in these markets may attract major investor attention.

Regulated Industries Are Hard

Financial services and insurance are not simple software categories. Compliance, licensing, carrier relationships, underwriting, consumer trust, and state-by-state regulation add complexity. A startup can have a great user interface and still face a mountain of operational challenges.

Strategic Investors Matter

Policygenius attracted not only venture firms but also insurance carriers and insurance-focused strategic investors. That matters because industry participants can provide credibility, partnerships, and distribution opportunities. In complex sectors, money is useful, but the right money is even better.

Funding Is Not the Same as Profit

A startup raising $276 million sounds glamorous. But capital raised is not revenue, profit, or shareholder return. Funding is fuel. If the engine is efficient, fuel helps the company go far. If the terrain gets rough, even a full tank can disappear quickly.

Experience-Based Perspective: What Policygenius Teaches Everyday Consumers and Founders

Looking at Policygenius from the outside, the most useful lesson is not simply “they raised a lot of money.” Plenty of companies raise money. Some become giants. Some become cautionary tales. Some become solid businesses inside larger companies. The more interesting lesson is how Policygenius approached a boring but important problem and made it easier for ordinary people to act.

Anyone who has ever shopped for life insurance knows the experience can feel strangely personal and painfully technical at the same time. You are thinking about your family, your income, your health, your debts, and your future. Then, suddenly, you are comparing policy terms, riders, underwriting classes, and medical exam requirements. It is emotional math, which is basically regular math wearing a heavier backpack.

A marketplace like Policygenius helps because it reduces the first big obstacle: confusion. When people do not understand a financial product, they often delay the decision. A young parent may know they need life insurance but keep postponing it because the process feels uncomfortable. A renter may ignore renters insurance because the monthly premium seems small enough to forget, until a pipe bursts upstairs and turns the apartment into an indoor splash pad.

From a consumer-experience perspective, Policygenius succeeded by meeting people where they were. It used plain-language content, comparison tools, and licensed experts to make insurance less mysterious. That is a valuable model for any financial business. If your customer needs a glossary, a calculator, and emotional reassurance before buying, your product is not just a product. It is an education journey.

For founders, Policygenius also shows why trust is expensive to build. You cannot simply launch an insurance marketplace and expect carriers, regulators, and consumers to immediately applaud. You need technology, compliance systems, partnerships, customer support, licensed professionals, marketing, and a brand that feels credible. That is one reason the company needed so much capital.

For investors, Policygenius is a reminder to separate product usefulness from investment outcome. A company can be useful and still face valuation pressure. A business can improve an industry and still not deliver the dream exit early investors imagined. Markets change. Interest rates change. Venture appetite changes. Public-company comparables change. The spreadsheet, unfortunately, does not care how elegant the mission statement sounds.

For personal finance readers, the practical takeaway is simple: use tools like insurance marketplaces, but do not outsource judgment completely. Compare quotes. Read policy details. Understand term length, coverage amount, exclusions, and conversion options. Ask whether you need life insurance at all, and if you do, whether term life is more appropriate than permanent coverage. The best insurance decision is not the one with the flashiest website. It is the one that fits your household’s risk, budget, and long-term plan.

The Policygenius funding story is ultimately a story about making financial protection easier to buy. The company raised more than $276 million because investors believed insurance distribution was overdue for modernization. Whether viewed as a startup story, an insurtech case study, or a consumer finance lesson, Policygenius proves one thing clearly: when an industry is confusing enough, making it simpler can become a very valuable business.

Conclusion

Policygenius has raised more than $276 million in publicly reported funding, with some databases estimating the total closer to $287 million or $288 million. Its biggest rounds were the $100 million Series D led by KKR in 2020 and the $125 million Series E in 2022, which included both venture investors and major insurance industry backers.

The company’s funding journey reflects the promise and difficulty of insurtech. Policygenius helped modernize how consumers compare and buy insurance, but it also operated in a complicated market shaped by regulation, underwriting, carrier relationships, capital cycles, and changing investor expectations. Its 2023 acquisition by Zinnia marked the next stage of the business, moving Policygenius from a standalone venture-backed marketplace into a broader insurance technology platform.

Note: Funding totals vary by source because some public databases classify financing rounds and credit facilities differently. This article uses the most commonly reported public figures and explains the range rather than presenting a single disputed number as absolute.