If you’ve ever stared at your credit report and thought, “Why is this ancient mistake still haunting me?” you’re not alone. The good news: most negative items are not allowed to sit on your credit report forever. Thanks to the Fair Credit Reporting Act (FCRA), there’s a credit reporting time limitusually seven yearsfor most bad marks. Once that clock runs out, those old debts are supposed to disappear from your reports like a bad haircut from your social media feed.

But what if they don’t? What if a collector is still reporting something that should have aged out years ago? Or what if an old, “zombie” debt suddenly comes back to life? In this guide, we’ll walk through how credit reporting time limits really work, what you can (and can’t) remove, and practical steps to clean up outdated debt information on your credit report.

How Long Do Old Debts Stay on Your Credit Report?

The FCRA sets clear limits on how long negative information can be reported. Federal agencies like the Consumer Financial Protection Bureau (CFPB), Federal Trade Commission (FTC), and major credit bureaus all agree on the basic framework: most negative items can stay on your credit report for up to seven years. Bankruptcies can stick around for longerup to ten years in some cases.

The general seven-year rule

- Late payments on credit cards, loans, and mortgages: up to seven years from the original date of delinquency (the first missed payment that led to the account going bad and never becoming current again).

- Collections accounts (paid or unpaid): up to seven years from that same original delinquency date on the original account, not from when it was sent to collections or sold to a new collector.

- Charge-offs, judgments, and similar adverse items: generally up to seven years under FCRA rules.

The 10-year exceptions

Some items get a longer stay on your financial “permanent record”:

- Chapter 7 bankruptcy: can be reported for up to 10 years from the filing date.

- Some other bankruptcies and certain judgments: often reported for seven years, but some credit bureaus or state rules allow up to 10 years.

Keep in mind: these are credit reporting limits. They don’t necessarily match how long a creditor can legally sue you to collect a debt. That’s governed by state statutes of limitations, which vary widely.

Credit Reporting Time Limit vs. Statute of Limitations

This is where people understandably get confused: there are two different clocks involved with old debts.

Clock #1: Credit reporting time limit

This controls how long a debt can appear on your credit report. For most debts, that’s seven years from the date of first delinquency. Once that time is up, the credit bureaus should stop reporting it.

Clock #2: Statute of limitations on debt collection

This governs how long a creditor or debt collector can legally sue you to collect. That time frame depends on:

- Your state

- The type of debt (credit card, auto loan, written contract, etc.)

Some states give collectors three or four years to sue; others allow more than ten years for certain types of contracts. After that window closes, the debt becomes “time-barred”they can still ask you to pay, but they generally can’t sue you if you assert the statute of limitations.

Here’s the key takeaway: even if a debt is too old for a lawsuit, it might still be on your credit report until the credit reporting time limit expires. And even after the reporting time limit has passed, collectors may still try to revive “zombie debt” by convincing you to make a small payment or acknowledge it in writingwhich can sometimes restart the statute-of-limitations clock in certain states.

When Old Debts Should Fall Off Your Credit Report

Under the FCRA, most negative items must be removed after they’re considered “outdated.” For most debts, that means:

Seven years from the date of first delinquency that led to the account never becoming current again.

That date is crucial. It’s not the date the account was placed in collections, the date it was sold to yet another collector, or the date someone updated the account. It’s the original missed payment date that started the downward slide.

Sometimes, however, outdated items don’t vanish on cue. Data entry errors, re-aging of accounts, or sloppy reporting can leave old debt information lingering on your credit report years after the legal reporting window closes. That’s when it’s time to take action.

Step-by-Step: How to Remove Old Debts After the Time Limit

1. Pull your credit reports (yes, all three)

You’re entitled to free credit reports from Equifax, Experian, and TransUnion through AnnualCreditReport.com. Review each report carefullysome old debts might appear on one report but not the others.

Look for:

- Collections that look ancient (six, seven, or more years old)

- Charge-offs older than seven years

- Bankruptcies older than ten years

- Duplicate listings of the same debt with multiple collectors

2. Identify the “date of first delinquency” (DOFD)

To know whether an item is past its reporting time limit, you need to find the DOFDthe first time you missed a payment and never brought the account current again. Consumer-law and compliance sources emphasize how critical this date is for FCRA compliance, specifically for determining when accounts should fall off.

If the DOFD is more than seven years old (or ten years for bankruptcy), the negative information is likely “outdated” and shouldn’t still be on your report.

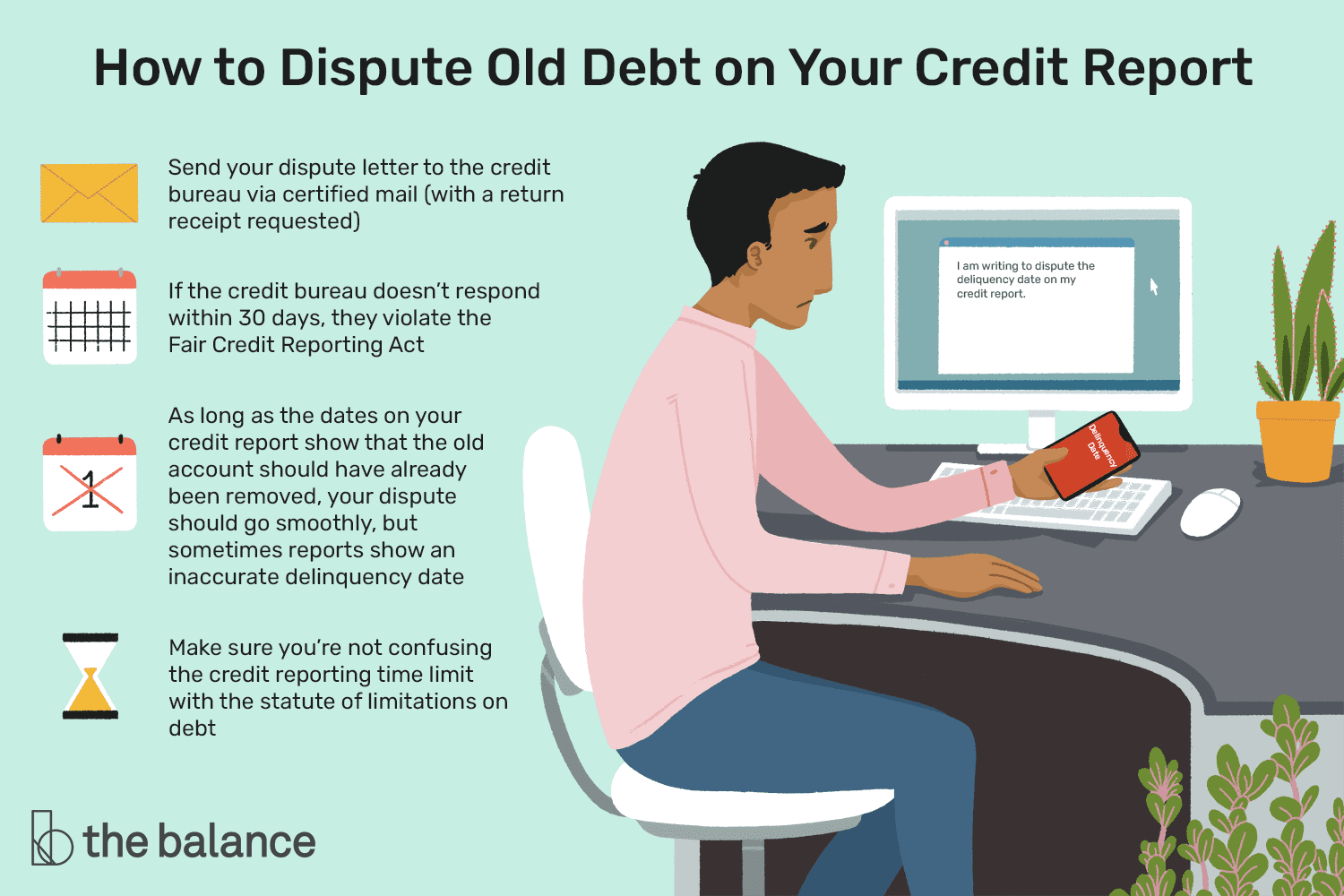

3. Dispute outdated information with the credit bureaus

Under the FCRA, you have the right to dispute inaccurate or outdated information. The basic process, as outlined by agencies like the FTC and credit bureaus themselves, looks like this:

- Write a dispute to each credit bureau reporting the outdated debt (Equifax, Experian, TransUnion). You can usually do this online, by mail, or by phone, but written disputes with documentation are often best for your records.

- Explain why the item is outdated. For example: “This collection account is more than seven years old based on a date of first delinquency of March 2017. Under the FCRA’s seven-year reporting limit, it should no longer appear on my credit report.”

- Include supporting documents if you have them: old statements, letters, or credit reports showing older dates.

- Keep copies of everything you send, and note the date of your dispute.

The credit bureau generally has about 30 days to investigate your dispute and respond. If they agree that the information is outdated, they must delete or correct it. If they don’t, they’re required to explain why they believe it’s accurate.

4. Dispute directly with the furnisher (optional but helpful)

You can also send a dispute to the company that furnished the informationsuch as the collector or original lenderespecially if the issue is a wrong date, duplicate account, or other reporting error. Consumer law guidance notes that furnishers also have responsibilities under the FCRA to report accurate, up-to-date information and respond to disputes.

5. Follow up if the item isn’t removed

If the credit bureaus refuse to remove an obviously outdated item, you have several options:

- File a second dispute with additional documentation.

- Submit a complaint to the CFPB describing the situation and attaching copies of your disputes.

- Consult a consumer law attorney if you believe your rights under the FCRA have been violated.

This is also where you want to keep your cool. Is it annoying? Absolutely. But organized documentation and persistence usually beat yelling at a call center.

What You Should NOT Do With Old Debts

Don’t accidentally “revive” zombie debt

“Zombie debt” is a nickname for very old, sometimes time-barred debt that debt collectors try to bring back from the dead. Articles from legal and consumer advocates warn that making even a small paymentor sometimes just acknowledging the debt in writingcan restart the statute-of-limitations clock in certain states.

Before paying on a very old debt:

- Find out whether the debt is within the statute of limitations in your state.

- Get details in writingwho owns the debt, the claimed amount, and your rights.

- Consider getting legal advice if you’re unsure.

Don’t agree to re-aged accounts

Some shady collectors may try to re-age an account by reporting a newer “date of first delinquency” or “date of last activity” to keep the account on your credit longer than allowed. That’s not just unfair; it can be illegal under FCRA rules.

If you see a collection account with a suspiciously new date even though the debt is old, that’s a red flag and a strong reason to dispute.

Be cautious with credit repair companies

Some companies offer to “wipe your credit clean” for a fee. Responsible credit repair services exist, but no one can legally remove accurate, timely negative information from your credit report. Trusted financial sources warn you to be skeptical of big promises, large upfront fees, or instructions to lie in disputes.

If you do use a credit repair company, make sure you understand your rights, the cost, and exactly what they’ll do on your behalf (hint: often the same disputes you can file yourself for free).

Life After Old Debts: Rebuilding Your Credit

Removing outdated or incorrect debt entries is powerfulbut it’s only half the story. Your credit score also depends heavily on what you’re doing right now. Credit education sources emphasize that as negative items age and ultimately fall off, consistent positive habits can help your score recover long before the full seven-year period ends.

Healthy habits to build a stronger credit profile

- Always pay on time. Payment history is a major factor in your score.

- Reduce credit card balances to improve your credit utilization ratio.

- Avoid opening too many new accounts in a short time.

- Keep older positive accounts open if possible to lengthen credit history.

- Monitor your credit regularly so you can catch errors earlybefore they age into problems.

Think of removing outdated debts as cleaning out a cluttered closet. It feels amazing to toss out what doesn’t belongbut the long-term magic comes from not shoving a new pile of junk in there next month.

Real-Life Experiences With Removing Old Debts

The rules are important, but sometimes it helps to walk through how this looks in real life. Here are a few composite examples based on situations many consumers face. (Names changed; stress levels very real.)

Case 1: The decade-old collection that refused to die

Maria pulled her credit reports while preparing to buy a home. To her surprise, a $450 medical collection from over eight years ago still showed up under a collection agency she’d never heard of.

Here’s what she did:

- Checked older records and learned the original bill was from 8.5 years ago, and the account had never been brought current.

- Confirmed the date of first delinquency was more than seven years in the past.

- Sent disputes to all three credit bureaus, explaining that the account was past the FCRA seven-year reporting limit and including a copy of an older credit report that listed the original delinquency date.

- Within about a month, two bureaus deleted the account. The third initially “verified” it, so she followed up, referencing the FCRA and attaching more documentation.

Result: the third bureau eventually removed the account as well. Her credit score jumped enough to qualify her for a better mortgage rate. The collection hadn’t been illegally re-aged on purposeit was simply sloppy data handling. But if she hadn’t challenged it, her interest rate might have been higher for years.

Case 2: The zombie credit card debt

James got a letter about an old credit card balance he hadn’t thought about in nearly a decade. The collection notice offered to “settle” if he made a small good-faith payment.

Instead of paying immediately, he:

- Checked his state’s statute of limitations and realized the debt was likely time-barred.

- Pulled his credit reports and saw that the collection account had already fallen off due to the seven-year reporting rule.

- Sent a written letter asking for validation of the debt and noting his understanding that it might be time-barred.

Had he paid or acknowledged the debt in the wrong way, he might have restarted the statute-of-limitations clock, opening the door to a lawsuit. Instead, he handled it cautiously and avoided accidentally reviving “zombie debt.”

Case 3: The “credit clean-up” year

Lena decided to treat her credit like a DIY renovation project. She had a handful of old late payments and a couple of collections, some of which were pushing the seven-year mark.

Over twelve months, she:

- Pulled her credit reports and highlighted anything older than six years.

- Verified DOFDs and flagged one collection that was already more than seven years from the first delinquency.

- Disputed that outdated collection, which was removed.

- Set up autopay to avoid any new late payments.

- Paid down credit card balances to under 30% utilization.

Even though not every negative item could be removed (some were still within the allowed time), removing the outdated one plus building new positive history gave her score a noticeable boost. She didn’t need perfectionjust progress.

What these experiences have in common

- They all started with understanding the credit reporting time limit and the importance of the date of first delinquency.

- Each person used their right to dispute information that was inaccurate or outdated.

- None of them relied on magic tricks or “secret loopholes”just the law, documentation, and persistence.

Your story may look different, but the core playbook is similar: know the rules, check the dates, dispute what doesn’t belong, and build better habits going forward. Old debts don’t have to define your financial future, and they certainly don’t get to live rent-free on your credit report forever.

As those outdated items finally fall off and your new habits kick in, your credit report starts to look less like a highlight reel of past mistakes and more like a story of recovery, resilience, and, yes, responsible adulting.