If the stock market had a guest list, most Americans would technically be invited. If the VIP table had a guest list, however, the names would get a lot more familiar: wealthy households, retirement funds, mutual funds, foreign investors, banks, insurance companies, pension plans, and a surprisingly large amount of paperwork wearing a tiny Wall Street necktie.

The question “Who owns all the stocks and bonds?” sounds simple, but it opens a trapdoor into the basement of modern finance. Stocks are not only owned by people clicking “buy” in a brokerage app. Bonds are not only owned by mysterious central bankers in dramatic lighting. Ownership moves through retirement accounts, index funds, insurance portfolios, college endowments, foreign reserve managers, broker-dealers, and custodians. In other words, the owner of a share of Apple or a U.S. Treasury bond may be a household, a pension fund, a university, a sovereign wealth fund, or your 401(k) quietly doing push-ups in the background.

This article breaks down stock ownership, bond ownership, and the big economic truth hiding underneath both: financial assets are widely accessible, but they are not evenly distributed.

The Fast Answer: Households Own a Lot, but Wealthy Households Own the Most

In the United States, households are the central owners of financial assets, especially through retirement accounts, mutual funds, exchange-traded funds, and brokerage accounts. But “households” is a very large bucket. It includes a teacher with a target-date retirement fund, a retiree holding municipal bonds, a young investor buying fractional shares, and a billionaire whose portfolio has more commas than a nervous English teacher.

Recent Federal Reserve distributional wealth data show that ownership of corporate equities and mutual fund shares is heavily concentrated. In the third quarter of 2025, the top 1% of U.S. households held about 50.2% of corporate equities and mutual fund shares. The next 9% held about 37.2%. The 50th to 90th wealth percentiles held about 11.6%, while the bottom half held around 1.1%.

That does not mean ordinary Americans are absent from the market. Gallup reported that 62% of Americans said they owned stock in 2025, including direct shares, mutual funds, or retirement accounts. SIFMA’s 2025 Capital Markets Fact Book also points to broad participation, noting that 58% of households owned equities in the latest Federal Reserve survey. The key distinction is participation versus percentage ownership. Many people are in the pool; a smaller group owns most of the water.

Who Owns Stocks?

1. Individual Investors

Individual investors own stocks directly through brokerage accounts, employee stock plans, dividend reinvestment plans, and mobile investing platforms. Some hold a few shares of a favorite company. Others hold concentrated portfolios worth millions. Direct stock ownership is easy to imagine because it feels personal: “I own shares of Microsoft,” “I bought Nvidia,” or “I invested in Coca-Cola because my fridge already did.”

But direct ownership is only part of the story. Many investors own stocks indirectly. They may never pick a single company, yet still own hundreds or thousands of stocks through a mutual fund, ETF, or retirement plan. A person contributing to an S&P 500 index fund owns a slice of 500 large U.S. companies without needing to know what all 500 do. Frankly, even some of the companies probably need a minute to explain what they do.

2. Retirement Accounts

Retirement accounts are one of the biggest gateways into stock ownership. A 401(k), IRA, 403(b), pension plan, or target-date fund often holds stocks and bonds through pooled investment vehicles. Investment Company Institute data show that tens of millions of U.S. households own mutual funds, and retirement savings are a major reason. In many cases, the average worker is not buying individual stocks; they are buying funds that own the stocks for them.

This is why the stock market matters beyond Wall Street. When the market rises or falls, it can affect retirement balances, pension funding, university endowments, nonprofit portfolios, and insurance reserves. The stock ticker is not just rich people confetti. It is connected to many long-term savings systems.

3. Mutual Funds and ETFs

Mutual funds and exchange-traded funds have become gigantic stock owners. They pool money from investors and buy baskets of securities. An index fund may own shares in nearly every major public company. An actively managed fund may choose a smaller set of stocks based on research, strategy, or the manager’s caffeine level.

Large asset managers often appear among the biggest shareholders of public companies because they manage funds on behalf of clients. This does not mean the asset manager personally owns all those shares in the ordinary sense. The economic exposure belongs to the investors in the funds: households, retirement plans, institutions, and advisers. The asset manager is more like the bus driver; the passengers own the trip.

4. Pension Funds, Endowments, and Foundations

Institutional investors are major owners of stocks. Public pension plans invest for teachers, firefighters, police officers, and government workers. Corporate pension plans invest for employees and retirees. University endowments invest to support scholarships, research, faculty positions, and buildings with names that sound like old law firms.

Foundations and nonprofits also own stocks to preserve and grow charitable assets. They may hold public equities, private funds, bonds, real estate, and alternative investments. For large institutions, stocks are not a hobby. They are part of a long-term funding engine.

5. Foreign Investors

Foreign investors own a major share of U.S. securities. U.S. Treasury survey data for June 30, 2025 measured foreign portfolio holdings of U.S. securities at about $35.349 trillion. That included roughly $19.860 trillion in U.S. equities, $13.840 trillion in long-term debt securities, and $1.649 trillion in short-term debt securities.

The biggest foreign investing locations included the United Kingdom, Cayman Islands, Canada, Japan, Luxembourg, and Ireland. These places are not always the final economic owners. Some are financial centers where global investors, funds, custodians, and institutions route holdings. So when a table says “Cayman Islands” or “Luxembourg,” it may be pointing to fund structures rather than a single national piggy bank sitting proudly on a beach chair.

Who Owns Bonds?

Bonds are IOUs. When you buy a bond, you are lending money to an issuer. The issuer might be the U.S. Treasury, a city, a state, a corporation, a federal agency, or a mortgage-backed security trust. In return, the issuer promises interest payments and repayment of principal, assuming all goes according to plan and no one trips over the legal documents.

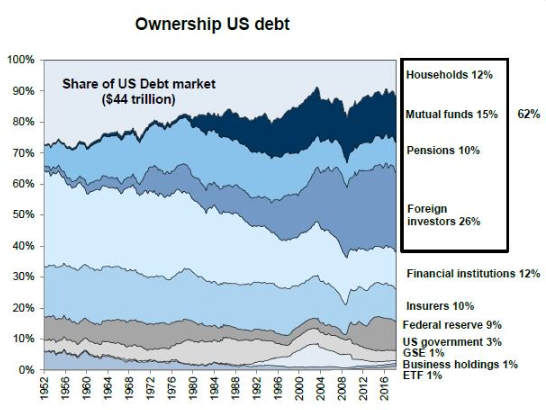

1. U.S. Treasury Securities

U.S. Treasury securities are owned by a wide range of buyers: households, mutual funds, money market funds, pension funds, banks, insurance companies, state and local governments, foreign investors, and the Federal Reserve. Treasury securities are considered among the safest and most liquid assets in the world, which is why they sit at the center of global finance like the financial system’s very serious sofa.

Foreign ownership is important but often misunderstood. Foreign investors hold trillions of dollars in U.S. Treasuries, but they do not own all U.S. debt. Domestic investors, U.S. institutions, retirement plans, banks, and the Federal Reserve are also major holders. As of early 2026 Treasury data, Japan, the United Kingdom, and mainland China were among the largest foreign holders of Treasury securities.

2. Corporate Bonds

Corporate bonds are issued by companies to borrow money. A company may issue bonds to expand operations, refinance debt, buy equipment, or fund acquisitions. Investors in corporate bonds include mutual funds, ETFs, insurance companies, pension funds, foreign investors, and households. Insurance companies are especially important bond buyers because they need predictable income streams to match long-term obligations.

Corporate bonds range from investment-grade debt issued by financially strong companies to high-yield bonds issued by riskier borrowers. The polite term is “high yield.” The less polite term is “please read the fine print twice.”

3. Municipal Bonds

Municipal bonds are issued by states, cities, counties, and public authorities. They can finance roads, schools, water systems, hospitals, airports, and other public projects. Many individual investors like municipal bonds because interest may be exempt from federal income tax, and sometimes state tax, depending on the bond and the investor’s residence.

Households, mutual funds, banks, and insurance companies are common municipal bond owners. For many retirees and high-income investors, municipal bonds serve as a relatively conservative income tool. They may not be glamorous, but neither is a sewer upgrade, and civilization seems pretty fond of both.

4. Bond Funds and Money Market Funds

Just as many people own stocks through funds, many own bonds through funds. Bond mutual funds and ETFs let investors gain exposure to hundreds or thousands of bonds. Money market funds often hold short-term Treasury bills, repurchase agreements, commercial paper, and other high-quality short-term instruments.

This matters because many investors do not personally choose individual bonds. Their retirement plan, brokerage account, or cash management account may own a fund that owns the bonds. The investor owns shares of the fund; the fund owns the underlying securities. It is ownership by financial nesting doll.

The Difference Between Record Ownership and Beneficial Ownership

Here is where things get delightfully weird. When you buy stocks through a brokerage account, your name usually does not appear directly on the company’s shareholder register. Most securities are held in “street name,” meaning the brokerage firm or another nominee appears as the registered holder, while you remain the beneficial owner.

Beneficial ownership means you get the economic benefits: dividends, gains or losses, voting rights passed through the broker, and account statements showing your holdings. Record ownership is the name officially listed on the books. This system makes trading faster and cheaper, but it also means the visible owner is often an intermediary.

So, if you ask, “Who owns this stock?” the answer might be: legally, a nominee or custodian; economically, millions of investors through brokerage accounts and funds. Finance: making simple questions wear tap shoes since forever.

Why Stock and Bond Ownership Is So Concentrated

Stock and bond ownership is concentrated for several reasons. First, higher-income households have more money left after paying for housing, food, childcare, transportation, medical costs, and the occasional emergency that arrives wearing steel-toed boots. More surplus income means more capacity to invest.

Second, wealth compounds. A household that owns assets early can reinvest dividends, interest, and gains. Over decades, the compounding effect can become powerful. A household with no savings has to climb the first hill before it can enjoy the downhill bicycle ride of compounding.

Third, retirement access differs. Workers with employer-sponsored plans often invest automatically through payroll deductions. Workers without a workplace retirement plan must take extra steps to open and fund accounts. Automation is underrated. It is the difference between “I invest every two weeks” and “I meant to invest, but then life tackled me in the cereal aisle.”

Fourth, financial knowledge and risk tolerance vary. People who grew up around investing may feel more comfortable owning funds, stocks, and bonds. Others may avoid markets because they seem confusing, risky, or designed by people who enjoy acronyms too much. Both reactions are understandable.

Do the Rich Own Everything?

No, but they own a very large share of financial assets. The top 10% of U.S. households own the overwhelming majority of corporate equities and mutual fund shares. They also own a large share of debt securities. This does not mean stock ownership is irrelevant for the middle class. It means the dollar value of ownership is very uneven.

For example, two households may both “own stocks.” One has $3,000 in a retirement fund. Another has $30 million across individual stocks, private funds, ETFs, and trusts. Both count as stock owners, but their market exposure is not remotely similar. One is holding a slice of pizza; the other owns the pizzeria, the delivery scooters, and possibly the oregano supplier.

Why This Ownership Map Matters

Understanding who owns stocks and bonds helps explain why financial markets influence the broader economy. When stock prices rise, households with larger portfolios benefit more. When bond yields rise, borrowers may face higher costs, but savers and income investors may receive better returns. When Treasury demand changes, it can influence government borrowing costs. When pension funds underperform, employers and governments may need to contribute more.

Ownership also shapes corporate governance. Shareholders vote on boards, executive pay, mergers, and proposals. When large funds own meaningful stakes in major companies, their voting policies can influence corporate behavior. At the same time, those funds are accountable to their own investors, whose money they manage.

The same is true in bonds. Bondholders may not vote on corporate directors, but they influence borrowing conditions. A company that wants to issue debt must satisfy buyers that the risk is worth the yield. If investors demand higher compensation, borrowing becomes more expensive. In that quiet way, bond owners have power too. They do not usually shout; they just ask for 75 more basis points and ruin someone’s afternoon.

Real-World Examples of Stock and Bond Ownership

The 401(k) Worker

Imagine a 35-year-old worker contributing to a target-date fund in a 401(k). That fund may own U.S. stocks, international stocks, Treasury bonds, corporate bonds, and cash equivalents. The worker may not know the names of all the securities, but they are still an owner through the fund. Their paycheck becomes capital for companies and governments.

The Retiree With Municipal Bonds

A retiree may own a municipal bond fund for tax-conscious income. That fund may help finance schools, transportation systems, or local infrastructure. The retiree receives income, and the municipality receives capital. It is not quite as thrilling as a superhero movie, but functioning water systems rarely get enough applause.

The Foreign Pension Fund

A pension fund in Canada, Japan, or Europe may own U.S. stocks and bonds because U.S. markets are large, liquid, and globally important. The ultimate beneficiaries could be nurses, teachers, engineers, or public workers in another country. So a share of a U.S. company may indirectly support retirement income on another continent.

The Insurance Company

An insurance company collects premiums and invests them, often in bonds, to meet future claims. When you buy insurance, part of that financial system flows into bond markets. The bond income helps insurers match long-term promises with long-term assets.

Experiences Related to “Who Owns All the Stocks & Bonds?”

The most practical experience connected to stock and bond ownership is the moment people realize they may already be investors without feeling like investors. Many workers open a retirement account, choose a default fund, and move on with life. Years later, they check the account and discover they own pieces of companies, government debt, corporate bonds, and international securities. It can feel like opening a closet and finding a tiny financial civilization living inside.

A common experience is confusion around ownership. Someone might say, “I do not own stocks,” because they have never bought an individual share. But if they have a 401(k), IRA, pension-linked investment, or mutual fund, they may own stocks indirectly. The same goes for bonds. Many people do not buy Treasury notes or municipal bonds directly, yet their money market fund, bond fund, or target-date fund may hold them every day.

Another experience is emotional. Stocks feel exciting because prices move visibly. Bonds feel boring until interest rates change, then suddenly everyone remembers bonds exist and starts using phrases like “duration risk” at dinner, which is one way to get fewer dinner invitations. Investors often learn that stocks and bonds play different roles. Stocks aim for growth and ownership in businesses. Bonds aim for income, stability, and repayment. Neither is magic. Both involve trade-offs.

Many families also experience the market through retirement conversations. Parents may worry whether their savings will last. Younger workers may wonder whether contributing small amounts matters. The ownership data can be both encouraging and sobering. It is encouraging because broad market participation is possible through low-cost funds and retirement plans. It is sobering because the largest gains flow to those who already own substantial assets. Starting earlier helps, but structural access matters too.

Small investors often describe their first market downturn as a lesson in ownership. When prices fall, a stock fund stops feeling like an abstract line on a screen and starts feeling like a roller coaster built by accountants. That experience teaches an important truth: owning securities means accepting uncertainty. The reward for taking risk is not guaranteed, but historically, diversified long-term ownership has been one of the main ways households build wealth.

There is also a civic experience hidden in bonds. When people buy Treasury bonds, municipal bonds, or bond funds, they are helping finance governments and public projects. A bond is not just a sterile financial object. It can be connected to roads, schools, utilities, hospitals, and public budgets. The owner receives interest; the issuer receives funding. That relationship is one of the quieter engines of modern society.

The final experience is perspective. Once you understand who owns stocks and bonds, headlines look different. “The market is up” no longer sounds like one giant scoreboard. It means households, pensions, funds, institutions, and foreign investors have seen asset values change. “Bond yields rose” no longer sounds like financial weather. It means borrowing costs, income opportunities, mortgage rates, and government financing conditions may be shifting. Ownership turns market news into human news.

Conclusion: Ownership Is Everywhere, but Not Equal

So, who owns all the stocks and bonds? The answer is: households, wealthy families, retirement savers, mutual funds, ETFs, pension funds, insurance companies, banks, endowments, foreign investors, governments, and central banks. But the deeper answer is more revealing: financial ownership is broad, layered, and highly concentrated.

Millions of Americans own stocks indirectly through retirement accounts and funds. Foreign investors own trillions in U.S. equities and debt. Institutions hold massive portfolios to fund pensions, insurance claims, scholarships, and public obligations. Yet the largest share of stock and bond wealth belongs to the wealthiest households.

That is the central lesson. Modern markets are not owned by one shadowy character in a leather chair. They are owned through a vast web of people and institutions. Some own a few threads. Some own ropes. Some own the loom. Understanding that web is the first step toward understanding how money, power, risk, and opportunity move through the economy.

Note: This article is an original SEO-focused draft based on public U.S. financial information from authoritative sources such as the Federal Reserve, U.S. Treasury, SIFMA, Investment Company Institute, SEC investor education materials, and major household ownership surveys.